Instrument Variable

category_specifier : "Causal Inference"

Reference Docs: Omitted Variable Bias | Endogeneity and Exogeneity

Motivation

💡I can’t run an experiment, but I want to know the causal effect.

- You lack a clean A/B test or random assignment.

- You suspect non-random selection into treatment.

- IV is a method born out of necessity - when experiments aren’t feasible and OLS is unreliable, IV becomes a powerful tool for credible causal inference.

The IV Solution

IV introduces a third variable (Z), the instrument, which:

- Is correlated with X (relevance) :

- Is not directly correlated with Y (exogeneity) :

This allows you to use only the part of X that is “as good as random” (driven by Z), isolating a causal estimate of \(\beta_1\).

When Do We Use IV?

Use IV when you suspect the explanatory variable (X) is correlated with the error term (e) in your model:

This breaks the OLS assumption and leads to biased estimates.

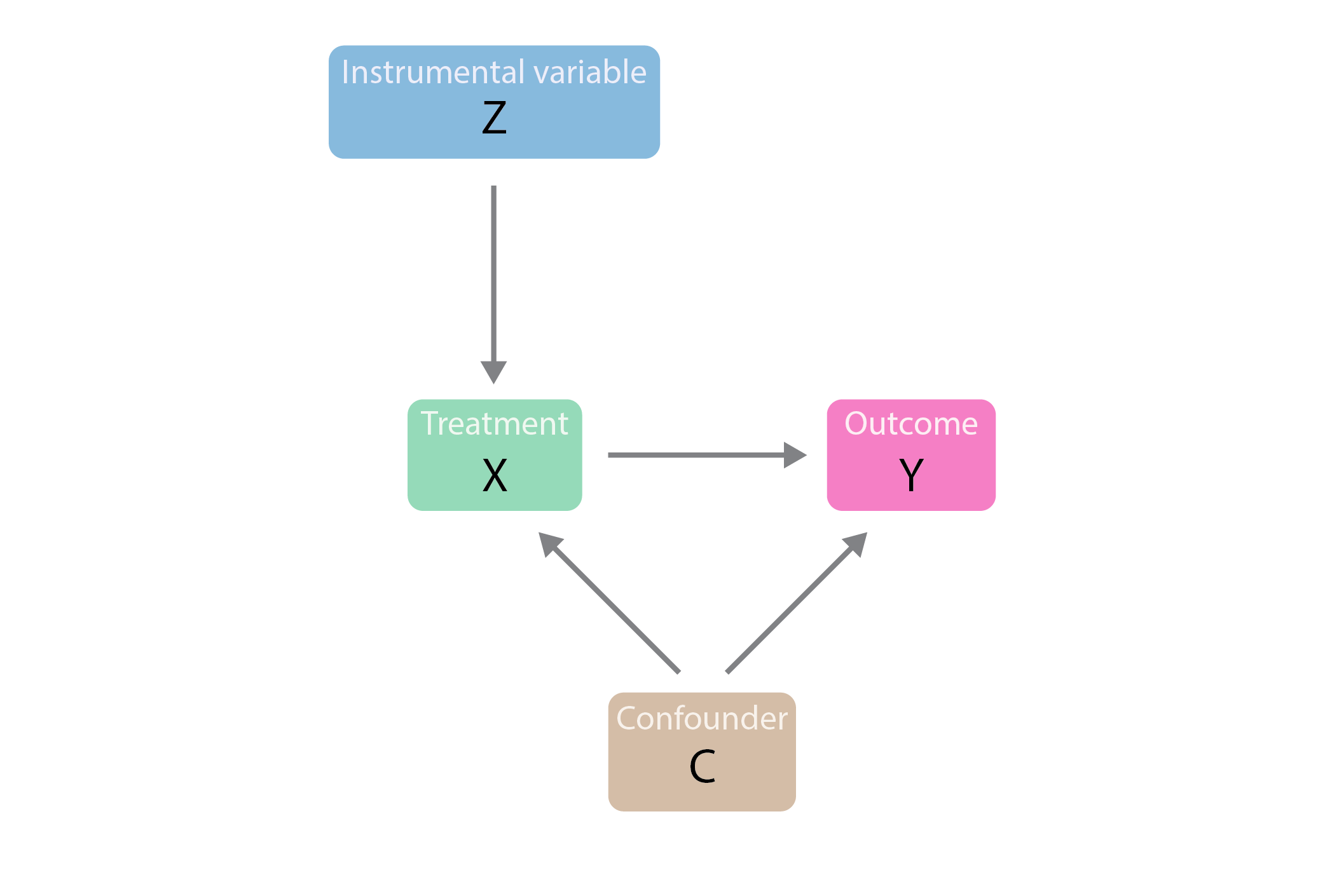

Visual Representation

In a causal graph:

- Z → X → Y

- Z → X must exist (relevance)

- Z → Y directly (exogeneity)

TSLS: Two-Stage Least Squares

A common IV estimation technique:

- First Stage:

Regress X on Z:

\(X = \pi_0 + \pi_1 Z + u\)

Use predicted \(\hat{X}\)

- Second Stage:

Regress Y on \(\hat{X}\)

\(Y = \beta_0 + \beta_1 \hat{X} + \epsilon\)

The estimated \(\beta_1\) is now unbiased, assuming instrument validity.

Examples & Use Cases

- Demand estimation: Use weather shocks or tax variation to instrument for prices.

- Crime and incarceration: Use prison overcrowding litigation as an instrument.

- Class size and student performance: Use earthquake-driven classroom reallocations.

- Birth weight and smoking: Use state-level cigarette prices as an instrument for maternal smoking.

Testing for Validity

- Relevance: Look at F-stat in the first stage. Rule of thumb: F > 10 is strong.

- Exogeneity: Testable only if you have more instruments than endogenous variables using the J-test (Sargan test).

Generalizations

- Can include multiple instruments and control variables.

- Must ensure the model is at least exactly identified (number of instruments ≥ number of endogenous regressors).

- Weak instruments bias TSLS toward OLS - use with caution!

Software Notes

- In Python: Use

IV2SLSfromlinearmodels.iv - In R: Use

ivregfrom theAERpackage